No Deadline: How to Reimburse Yourself From Your HSA Years Later, Tax-Free

There's no deadline to reimburse yourself from your HSA. Pay out of pocket now, let the money grow invested, and pull it out tax-free years later — if you kept the receipt.

You've probably heard you can reimburse yourself from your HSA. Maybe you even tried once — found the expense, went looking for the receipt, hit a form asking for details you didn't have, and gave up halfway. So you did what most people do: swiped a regular card for the copay and told yourself you'd sort out the HSA part later. Later never came.

Here's what that form didn't tell you: the money isn't lost. You can pay yourself back for qualified medical expenses years after you paid them — there's no deadline at all — as long as you kept the receipt. The HSA doesn't have a clock on it.

The fast answer: how reimbursing yourself works

Reimbursing yourself from a Health Savings Account (HSA — a pre-tax account tied to a high-deductible health plan) is simple once you see it: pay for a qualified medical expense out of pocket today, leave the HSA invested so it grows, and claim the money back whenever you want — next month or in 2046. There's no deadline to do it. The only catch is proof: you need the receipt when you finally pull the money out.

TL;DR: Pay out of pocket now, let the HSA grow, and reimburse yourself any time later — there's no deadline, as long as you saved the receipt.

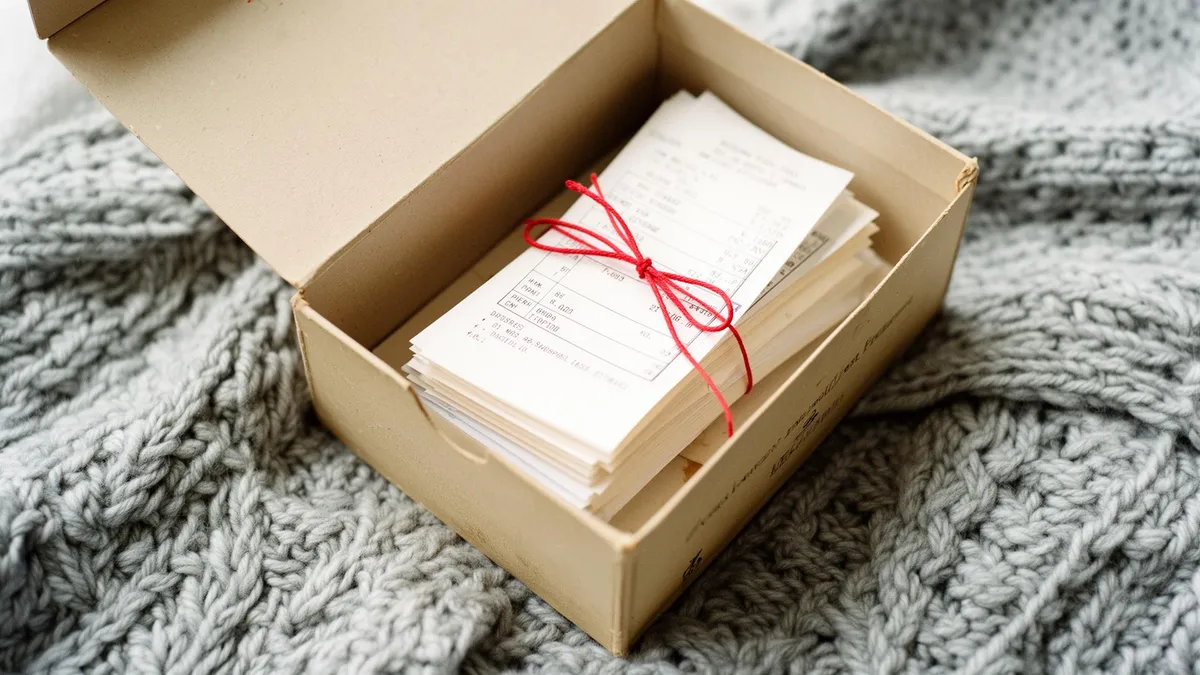

First, a concept worth knowing: the “shoebox” approach

There's an old nickname for this: the “shoebox” approach. People saved every medical receipt in a shoebox, left their HSA invested for years, and reimbursed themselves much later. The shoebox was always just the receipts — the growth is the point. The problem was never the idea; it was keeping a decade of paper findable.

Sometimes paying with a credit card is the smart play — it lets your HSA keep growing tax-free, and you might earn card points along the way. The catch has always been proving the expense when you finally reimburse yourself.

That's what Caeli's Smart Shoebox is built for: it vaults every Buy-with-Benefits purchase — itemized, auto-labeled with the reimbursable amount and program, and paired with a Letter of Medical Necessity whenever one applies. Years from now, you pull up a single purchase or a whole year's worth in bulk, and reimbursing yourself is one tap. The receipts keep themselves.

Your 30-second cheat sheet

The three rules that make it legal

- The expense came after you opened the HSA. You can't reimburse yourself for something from before the account existed.

- You weren't reimbursed any other way. Insurance didn't already cover it, and you didn't use an FSA for the same expense.

- You didn't deduct it on your taxes. You can't take the medical-expense itemized deduction and reimburse from your HSA for the same cost.

The one habit that makes it work

Keep every receipt, indefinitely. The IRS doesn't collect them when you file — the burden is on you to produce them if you're ever audited. No receipt, no defensible reimbursement.

TL;DR: After the account opened, not otherwise reimbursed, not deducted — and keep the receipt forever.

How do you actually pay yourself back?

The mechanics are almost anticlimactic. Log into your HSA provider, find the reimbursement or “pay yourself back” option, enter the expense amount and date, and choose how you want the money: an electronic transfer to your bank, or a check. Most providers let you attach the receipt right there so it lives with the record. The cash usually lands in a few business days.

To reimburse yourself, you need an itemized record showing what was bought, that it was a qualified medical expense, and when. If you bought it through Caeli, that record already exists — your Smart Shoebox has the itemized receipt filed and labeled, so the decade-old expense you're hunting for is one search.

Why would anyone wait years to get their own money?

Because the waiting is what makes it pay. Three real reasons people deliberately delay:

- Tax-free growth. Money left in the HSA can be invested and compounds without being taxed. The longer you leave your own reimbursement sitting in the account, the more it earns on your behalf.

- A flexible emergency reserve. Years of saved receipts become a pool of tax-free cash you can summon whenever you need it. Big unexpected bill? Reimburse yourself for a stack of old expenses and pull out a lump sum, tax-free, on your schedule.

- Retirement income. This is the long game, and it deserves its own piece — the HSA can function as a stealth retirement account. We go deep on that in our guide to the HSA triple tax advantage. This article stays focused on the mechanics of paying yourself back.

The rules that trip people up

The expense has to come after your HSA was established. This is the one people miss most. A medical bill from before you opened the account can't be reimbursed — even by a day. If you're opening an HSA now, the clock on this strategy starts today, not retroactively.

It must be a qualified medical expense. The cost has to be one the IRS recognizes — the same categories that would qualify for the medical expense deduction. Dual-purpose items (a massage gun, an air purifier) may need a Letter of Medical Necessity to count; we cover that in our guide to Letters of Medical Necessity. Caeli checks your plan's eligibility rules at checkout, so the things you're filing away as future reimbursements were actually eligible when you bought them.

No double-dipping. You can't reimburse from the HSA for an expense you already covered with an FSA, that insurance paid, or that you claimed as a tax deduction. Pick one path per dollar.

If you reimburse by mistake, you can usually fix it. Pull money for something that turns out ineligible and you can return it as a “mistaken distribution” — generally by the next year's tax-filing deadline — to avoid tax and the 20% penalty. After 65, withdrawals for non-medical things skip the penalty but still count as taxable income.

TL;DR: Expense must post-date the account, be genuinely qualified, and never be reimbursed twice. Honest mistakes are fixable if you catch them in time.

What you actually need to keep

An itemized receipt showing the date, what was purchased, and the amount. A credit card statement alone usually isn't enough — “PHARMACY $42.18” doesn't prove what you bought. For anything that needed a Letter of Medical Necessity, keep the letter paired with the receipt. And hang onto all of it for at least three years after the tax year you finally take the reimbursement — longer is safer, since you may be reimbursing decades out.

This is the unglamorous heart of the whole strategy, and it's where good intentions go to die in a junk drawer. A record-keeping system you'll actually maintain for 20 years is worth more than the cleverest tax plan you abandon in month three. Caeli auto-archives every receipt and its matching Letter of Medical Necessity in one place, so the documentation for a reimbursement you make in 2045 is already sitting there, organized, today.

Frequently asked questions

Can I reimburse myself from my HSA for an expense from several years ago?

Yes. There's no time limit on HSA reimbursements. As long as the expense was a qualified medical cost incurred after you opened the HSA, wasn't reimbursed another way, and wasn't deducted on your taxes, you can pay yourself back years — even decades — later. The only requirement is that you kept the receipt.

Is there a deadline to reimburse yourself from an HSA in 2026?

No. As of 2026 the IRS still places no deadline on HSA reimbursements. You can let qualified expenses accumulate for years and reimburse yourself whenever it suits you — which is exactly what makes the shoebox approach work.

Does the medical expense have to be from after I opened my HSA?

Yes, and this is the rule people most often get wrong. Only expenses incurred on or after the date your HSA was established are eligible for reimbursement. A bill from before the account existed can't be paid back from it — so if you're opening an HSA now, start saving receipts from today forward.

Do I need to keep paper receipts, or is a bank statement enough?

You need an itemized receipt showing the date, the item, and the amount. A bank or credit card statement usually isn't sufficient on its own because it doesn't prove what you actually bought. Digital copies are fine — what matters is that the documentation is itemized and that you can produce it if audited.

What happens if I reimburse myself for something that wasn't actually eligible?

If you catch it, you can usually return the money as a “mistaken distribution” — generally by the tax-filing deadline of the following year — and avoid tax and the 20% penalty. If you don't fix it, the amount is taxed as income plus a 20% penalty (the penalty disappears after age 65, but income tax still applies).

Can I still reimburse myself from my HSA after age 65?

Yes. Reimbursing yourself for qualified medical expenses stays tax-free at any age. After 65 you can also withdraw HSA funds for non-medical reasons without the 20% penalty — though those non-medical withdrawals are taxed as ordinary income, much like a traditional retirement account.

Bottom line

Every qualified medical expense you pay out of pocket — and document — is a tax-free withdrawal you've given yourself permission to take whenever you want. Those copays you paid out of pocket weren't lost. They were IOUs you never cashed, just sitting there while the money that could have covered them kept growing instead.

The shoebox was always just a way to keep the receipts. What you really need is a habit you'll actually keep and proof you can find years later. Get that right, and your HSA becomes one of the most flexible tax-free accounts you'll ever hold.

Install Caeli and let it keep your receipts and Letters of Medical Necessity paired and audit-ready — so the money you pay yourself back years from now is already documented today.

TL;DR: No deadline, no lost money — just keep itemized proof. Document today, reimburse whenever, take it out tax-free.

Put it to Practice

Vetted brands & products

Recommendations we genuinely stand behind — vetted for quality and benefit eligibility.

Continue learning

All articles

Benefits Maxing

The Art of Benefit Stacking: How to Get a Net-Zero Wellness Lifestyle

When your HSA, FSA, LSA, and credit card rewards work together, a $200 gym setup can effectively cost $0. Here's how the stacking math actually works.

Benefits Basics

Does "Eligible" Mean "Approved"? FSA & HSA Card Swipes, Explained

A successful FSA card swipe isn't the same as an approved expense. Here's the difference between eligible and approved — and how to get reimbursed cleanly the first time.

Caeli Picks

Your Wellness Stipend Probably Pays for Peloton, ClassPass, and Your Gym

Your employer's wellness stipend (LSA) likely covers Peloton, ClassPass, gym memberships, and Calm — if you spend it before year-end. Here's what an LSA actually pays for.